Because the economy stopped growing, which means there is little demand for money. If there is a large demand for capital then interest rates will rise. It's ordinary supply and demand only applied to money rather than some good or service.

I guess it depends on which side you are thinking from in arguments like these. The interest rate a bank will give you depends on how much demand there is for the money that you are about to give that bank. If the bank has no way to make a profit on the money they give you because there is little demand then they will offer you a low interest percentage (or even none or a negative one).

So yes, there is an oversupply, but that's the same as little demand on the other side of the bank, plus or minus some arbitrary skew in time.

The bank simply tries to make money from being in the middle between supplier of capital (you and your savings) and the consumers of capital (the demand side, industry, mortgages and so on).

The monetary system hasn't been about 'me and my savings', for at least 3 decades. Reasoning about banks, capital, supply/demand, return on investment, in terms of whether consumers spend their savings or leave it sitting on a bank account, will not make you any wiser about the state of the economy or our monetary system.

Current rates are low because central banks everywhere are basically flooding the world with free money, throwing good money after bad money by monetizing poisonous debt, to prevent the financial system from imploding (which almost happened in 2008). Or at least postpone it for as long as possible. Ben Bernanke will be (almost) the last person on earth to say this out loud, which makes the value of this fluff piece on a site like this pretty dubious. There's a reason why his nickname is 'Helicopter Ben'.

This could not be more wrong. Current central bank rates are high compared to market rates for stores of value, otherwise people, banks and businesses would not be keeping so much of their savings in idle excess fiat.

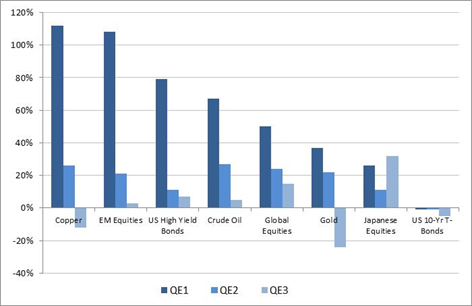

Eh? The Federal funds rate has been at 0.25% since 2008, if it were to go any lower we'd be in negative interest rate territory. The fed has only just started scaling back their asset repurchase program (aka 'QE' for 'quantitative easing'), but just like the previous 3 times (in ~5 years) it supposedly wanted to stop 'printing money', another round of QE is just one big stock market correction or housing market crash away. All the FED did to 'improve the economy' through its actions is drive up the stock market, create opportunities for malinvestments (e.g. the shale oil industry that is now about to collapse because of lower oil prices), and drive other central banks around the world to do the same to avoid their currencies decoupling too much from the value of the dollar. Things don't look too bad right now because most of the rest of the world (except Japan) is basically about a year behind the curve compared to the US, and we the next powder keg hasn't exploded yet, but the fuse has been lit, and it's just a matter of time until Bernanke will have to eat his words and all the asset bubbles the Fed created under his supervision explode in the faces of all these retirees he was supposedly so concerned about...

Just to be clear, I'm not saying Bernanke had easy and/or painless other policy options, or that central banks would even have the ability to fix the global economy and monetary system by the way. Just that a piece like this is a more or less meaningless bedtime story.

Risk adjusted market returns are clearly in negative territory otherwise we wouldn't have these piles of idle reserves even at -2% real return.

> for malinvestments (e.g. the shale oil industry...

Malinvestment is not something that exists under any mathematically consistent macroeconomic model but even if we try to tie the word to a somewhat sensical meaning, the most "malinvested" form of savings, short of using the money to hire people to destroy property, is to keep the savings as excess idle money. Savings have a return of near -100% to the aggregate economy when they are turned into uninvested idle fiat. The returns are even lower than -100% if you consider the welfare paid to the unemployed this results in.

Even if the shale oil industry gets a very poor return of -50% it would still be better for economic value creation than building excess fiat. Of course central banks did not cause the shale oil troubles as they set their rate to imply anything not having at least -2% risk adjusted real returns is not worth doing. Shale oil went way below that because of factors independent of central banks.

If a monetary bubble ends up bursting it will be because central banks have been too tight, making fiat keep its value above market safe returns and getting people and banks to stockpile it instead of investing in the private economy, effectively turning savings into mere intrinsically valueless paper which doesn't have any economic activity, any stuff or means of production to back them.

That's definitely a good point, but even a madman with a printer counts as 'supply outweighing demand'. The principles don't really change. That's why printing all this money is going to catch up with us sooner or later.

>That's why printing all this money is going to catch up with us sooner or later.

In 2009, here on HN, people were warning that the first round of QE would lead to Weimar-style hyperinflation in fairly short order. Six years and two additional rounds of QE later, interest rates and inflation in the U.S. are still quite low.

People tend to forget that the economy has done quite well even under inflation levels that we'd now consider high; during the Reagan boom, inflation fluctuated between 3-5%. Even if all this QE led to 5% inflation for a number of years, that's not really a serious problem (and certainly not hyperinflation).

It starts to get painful when you get to 10%, 15%, 20%, but that's a fixable problem. Indeed, it was fixed at the end of the 1970s. It was painful, but it was fixed.

So, yes, it might catch up with us. But when and how badly matter a lot. If the cost of all this QE is that average inflation in the 2020s is 5%, so what? That's hardly a disaster. Or let's say inflation creeps up to about 12%, and in 2025 the Fed takes strong action to get it under control, leading to a sharp painful recession in 2025-26. Should we have a decade or two's worth of stagnation to avoid this hypothetical? I personally don't think so.

Maybe but it's central banks being to timid in printing money, making it too valuable and increasing the demand for it that ends up making them print much more just to barely keep the economy going. They are making fiat so valuable that it displaces private investment as a store of value and money accumulates in the economy as idle excess reserves.

If central banks had printed sufficiently and promised to push inflation high enough early in the financial crisis, the market would have cleared and much less money would have accumulated idle in the system overall.

This is a false understanding of how the supply and demand for money works. For example, news about QE was positively correlated with long term interest rates. The expectation of an increased future money supply tilted the balance towards the demand side in the present.

Money is fundamentally an intertemporal thing, and we've known since the 1930s that the cute little supply-demand time-slice diagrams in textbooks don't work on the money supply.

I'm not sure I follow. The Federal Reserve has manipulated the interest rates and money supply since 1913. The money market demand can't help determine the supply of money since the cost of money is the interest rate. Consumers aren't allowed to see if its worth while to save their money and earn interest rather than spend their money. Businesses can't see if its worth it to focus on current production or invest in infrastructure for future production because of artificial rates.

Although you got the sign right, that is the rising supply of money does lower interest rates, in most of the world there is certainly not an oversupply.

Money at around -2% real return is still pricing private stores of value, read new investment, out of the market. Money needs a real return that is lower than that so that fiat is not over valued compared to market stores of value, and people, banks and businesses don't hold their savings in excess idle reserves instead of in things that have intrinsic value and that are backed by economic activity.

{kind=link}